ROTH isn’t the only way to achieve tax-free income

Everyone Loves Roth IRAs… Because They Hate Taxes. But How Can You Avoid Federal Tax on Stock Sales Without One?

In 2011, Warren Buffett made headlines when he said he paid a lower tax rate than his secretary. It wasn’t because he was cheating the system. It was because most of his income came from long-term capital gains, while his secretary’s income was taxed as ordinary wages. Buffett wasn’t gaming the system. Rather, he was using it in the way it was designed and so can you.

Ask any investor why they love their Roth IRA, and the answer is almost always some variation of, “Well, it grows tax-free, and I don’t have to pay taxes when I take the money out.” Hard to argue with that. But here’s the secret that most investors don’t realize: you can replicate much of what makes a Roth so powerful without one.

When advisors talk about retirement savings, they usually prioritize 401(k)s, 403(b)s, IRAs, and so on. Taxable accounts? Those come last, once you’ve “maxed everything else out.”

However, a taxable brokerage account can be one of the most tax-efficient tools in retirement. You see, the government designed the tax code to encourage investment activity by providing preferential tax rates on long-term capital gains, which is the tax you pay on profits from investments like stocks, ETFs, property, etc., held greater than one year.

Let me elaborate.

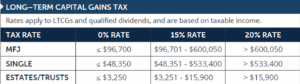

For 2025, if you’re married filing jointly (MFJ) and your taxable income is $96,700 or below, the federal tax rate on long-term capital gains is 0%. That’s right! Zero. Zip. Nada.

I’ll say it again: if you and your spouse’s taxable income is $96,700 or lower, any long-term capital gains are taxed at 0%.

Let’s say that you made the smart decision together years ago to invest in Apple stock and bought $25,000 worth. Now, its worth $150,000 and you plan to sell… thus, the total long-term capital gain would be $125,000. If this is your only source of income for the year, you will have:

- $125,000 in Long-Term Capital gains – $30,000 standard deduction = $95,000 in taxable income

Because your taxable income is below the threshold of $96,700, you pay no federal income tax, no Social Security or Medicare tax, and to sweeten the deal, should you be in a state like AK, FL, NV, SD, TX, TN, WY, or NH, you pay no state income tax…on ANY of your long-term capital gain.

Walser Wealth can help with variants of this approach. For example:

- Pull $25k from 401(k)

- Pull $50,000 in long term capital gains from a taxable brokerage account

- Receive $10,000 in qualified dividends from a taxable brokerage account

- Pull $25,000 from a Roth IRA

= $0 in federal tax BUT $110,000 of net cash

Yes, really!

Keep in mind that if you are single, this strategy still works with taxable income up to $48,350 using a standard deduction of $15,000 (vs. $30,000 for MFJ).

To give you another example, let’s say you and your spouse, both age 62, retire early. You’re healthy, your mortgage is gone, the kids are out of the house, and you’ve got some savings spread across IRAs and a brokerage account. You decide to delay Social Security until age 70 to maximize your monthly benefit.

Now what?

You’ve just entered one of the most overlooked, tax-efficient windows of your life. With your income temporarily low, you have room to:

- Convert money from your traditional IRA to a Roth IRA—paying little or no tax.

- Sell appreciated investments from your brokerage account—again, potentially paying no tax.

Let’s say you convert $30,000 from your IRA to a Roth. That’s taxed as ordinary income. Then, you sell $96,700 worth of stock that you’ve held in a taxable brokerage account for over a year, realizing a long-term capital gain. Your total income for the year is $126,700. Subtract the $30,000 standard deduction, and your taxable income is right at $96,700—the top of the 0% capital gains bracket.

You just converted $30,000 to a Roth and took $96,700 in long-term capital gains income. Your total federal tax bill? $0.

What makes this strategy so powerful isn’t just the tax savings but the flexibility. You decide when to take income. You decide how much to convert. You decide when to sell. You’re not at the mercy of a paycheck or a required minimum distribution (RMD). And we certainly can’t forget about capital losses, as they can be just as useful as gains. Selling a loser in your portfolio to offset a gain—even if you still like the company—can create room to take additional cash without exceeding the taxable income threshold. This “tax alpha” may not show up in performance charts, but it absolutely adds real value over time.

For years, clients have been told that Roths are the holy grail of retirement tax planning. And they’re great, but they’re not the only game in town. A taxable brokerage can provide incredible outcomes when paired with intentional planning.

So, let’s help you take advantage of it!

By: Russell Becker, CFP®

Published on 8/25/25